I

would like to present a simple R code which can load tweets timelines of

specified users, then, in the loaded tweets, find frequent terms, some associations

with specified terms and display the results as terms clouds. I think such

visualization is more effective for sentiment analysis if compared with the

calculation of positive and negative words, and it can give more intuitive tips

for analytics. Users

can use the following functions: gettweets(), freqterms(), assoc("term"), stock("symbol").

The

gettweets() function allows users to load the latest tweets from a

specified list of twitter users, such as: CNN, WSJ, Reuters, Bloomberg, etc.

Please, use this function only once per analysis, because if you load tweets

too often, Twitter can block you IP. With

the following command, you can specify the maximum number of latest tweets that

can be loaded from each user's timeline:

gettweets(number), the default number is 100. The function freqterms() will output more

frequent terms.

The

function assoc("term") will display the terms that are correlated

with some specified term, e.g. assoc("apple").

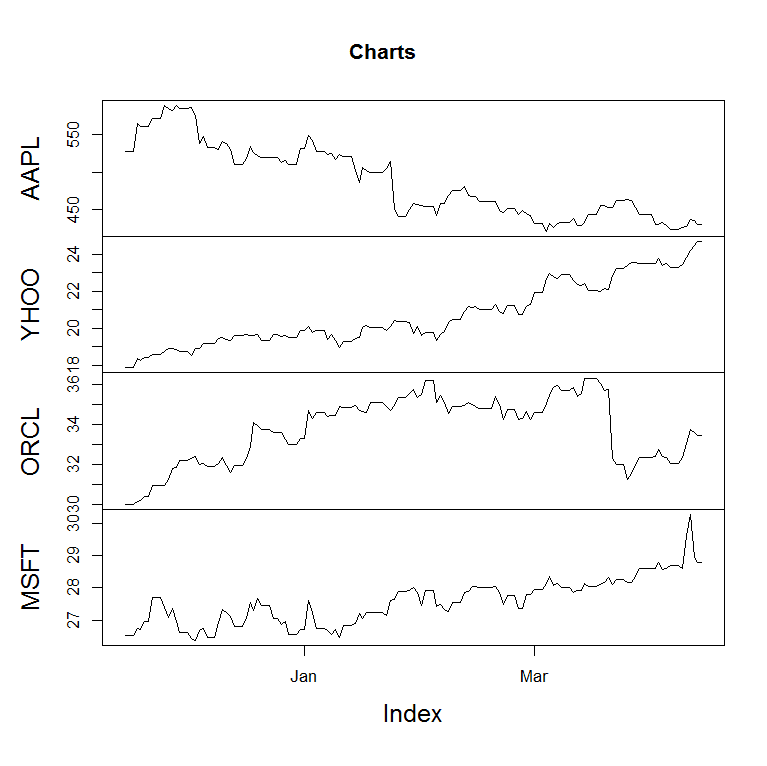

The

function stock("symbol") will display a stock chart for some

specified symbol, a cloud of terms which are correlated with the specified

symbols, and the forecasting, based on the ARIMA model. Each company has its

own specified symbol, e.g.: Google - GOOG, Apple - AAPL, Yahoo - YHOO, Dell -

DELL, Oracle - ORCL, Microsoft - MSFT, Cisco - CSCO, etc. For example, the function stock("GOOG")

will display a stock chart fro Google.

Download R-code

To

work with this program, you need to install R (more info at http://r-project.org). Before

starting the program, you need to install the additional packages, you can do

this using the following commands:

install.packages("twitteR")

install.packages("tm")

install.packages("RJSONIO")

install.packages ("forecast")

install.packages ("quantmod")

Our

next step is going to be the use of multivariate forecasting algorithms based

on the vector ARMA model. These algorithms can include many time series into analyses,

the time series describe both stock prices and quantitative characteristics of

tweets. I think such an approach will give the narrower and more precise

forecasting. To the effective tweets characteristics, we are planning to use

the theory of semantic fields, frequent sets, associative rules, Galois

lattice, the formal concepts analysis. Such an approach can be found in our

previous investigations at

http://arxiv.org/ftp/arxiv/papers/1302/1302.2131.pdf

http://bpavlyshenko.blogspot.com/2012/12/the-model-of-semantic-concepts-lattice.html

http://bpavlyshenko.blogspot.com/2012/12/investigation-of-concept-end-of-world.html

http://bpavlyshenko.blogspot.com/2013/01/data-mining-of-concept-end-of-world-in.html

Please write your comments.

Printscreens of functions performing:

gettweets():

freqterms():

assoc("apple"):

stock("GOOG"):